Home Reversion Calculator: Understand Your Home’s Value with a Reversion Calculator

Home reversion is a financial scheme that allows homeowners to release equity from their property without the need to move out. One of the essential tools in understanding this process is a home reversion calculator. This tool helps you estimate the value of your property and how much equity you can release. It is beneficial for those considering home reversion as it provides a clear picture of potential financial outcomes. This article will delve into the details of using a home reversion calculator, its benefits, and how it can aid in making an informed decision about your home's value.

Maximizing Your Home's Potential: The Benefits of Using a Home Reversion Calculator

A Home Reversion Calculator is a powerful tool that can help you understand the potential value of your home should you decide to go into a home reversion scheme. This calculator takes into account a variety of factors such as your age, your property's value, and the percentage of your property you wish to sell, and provides an estimate of how much money you could receive.

What is Home Reversion?

Home reversion is a type of equity release scheme where you sell a portion or all of your home to a home reversion company in exchange for a lump sum of money or regular payments. You can continue to live in your home rent-free until you pass away or move into long-term care.

How Does a Home Reversion Calculator Work?

A Home Reversion Calculator works by taking into account a variety of factors, including your age, your property's value, and the percentage of your property you wish to sell. It then uses these factors to calculate an estimate of how much money you could receive from a home reversion scheme. This can help you make an informed decision about whether a home reversion scheme is right for you.

Why Should You Use a Home Reversion Calculator?

There are many reasons why you should use a Home Reversion Calculator. First, it can help you understand the potential value of your home and how much money you could receive from a home reversion scheme. Second, it can help you compare different home reversion schemes and find the one that best suits your needs. Finally, it can help you make an informed decision about whether a home reversion scheme is right for you.

What Factors Affect the Results of a Home Reversion Calculator?

The results of a Home Reversion Calculator can be affected by a variety of factors, including your age, your property's value, and the percentage of your property you wish to sell. Typically, the older you are and the more valuable your property is, the more money you could receive from a home reversion scheme. However, the exact amount will depend on the specific home reversion scheme you choose.

How to Use a Home Reversion Calculator

Using a Home Reversion Calculator is simple. All you need to do is input some basic information about yourself and your property, including your age, your property's value, and the percentage of your property you wish to sell. The calculator will then provide an estimate of how much money you could receive from a home reversion scheme.

| Factor | Description |

|---|---|

| Age | The older you are, the more money you could potentially receive from a home reversion scheme. |

| Property's Value | The more valuable your property is, the more money you could potentially receive from a home reversion scheme. |

| Percentage of Property to Sell | The more of your property you wish to sell, the more money you could potentially receive from a home reversion scheme. |

How to calculate home reversion?

To calculate home reversion, you need to understand that it is a type of equity release scheme where you sell a portion of your property to a home reversion provider in exchange for a lump sum or regular payments. The amount you receive will be less than the market value of the share you sell because you retain the right to live in the property rent-free for the rest of your life or until you move into long-term care.

Home reversion plan calculator

Understanding Home Reversion

Home reversion is a way for older homeowners to access the equity in their property without having to move out. The key points to understand about home reversion are:

- Partial sale: You sell a portion of your property, not the entire thing.

- Discounted value: The provider pays less than the market value for the share they purchase.

- Lifetime tenure: You can live in the property rent-free for the rest of your life.

Calculating the Home Reversion Amount

The amount you receive from a home reversion plan depends on several factors:

- Age: The older you are, the more you can typically receive.

- Property value: A higher property value usually means a larger sum.

- Share sold: The proportion of the property you sell directly affects the amount received.

Considering the Pros and Cons

Before deciding on a home reversion plan, it's essential to weigh the advantages and disadvantages:

- Pros: You can access a lump sum or regular payments while continuing to live in your home rent-free.

- Cons: You will receive less than the market value for the share of the property you sell, and the provider will benefit from any future increase in property value.

- Irreversibility: Home reversion is a significant decision that can be difficult or impossible to reverse.

What are the disadvantages of home reversion?

The disadvantages of home reversion are numerous and can have a significant impact on homeowners considering this option. Home reversion involves selling a portion or all of your property to a company in exchange for a lump sum or regular payments, while retaining the right to live in the property for the rest of your life or until you die. While it can provide a source of income, there are several drawbacks to be aware of.

Limited Ownership and Control

One of the main disadvantages of home reversion is that homeowners give up ownership and control of their property. This means they no longer have the right to make decisions about the property, such as renovations or selling. Additionally, the company that purchases the property may impose restrictions on how the property is used.

- Loss of ownership rights: Home reversion requires selling a portion or all of your property, which means giving up the rights to make decisions about it.

- Limited control over property use: The purchasing company may impose restrictions on how the property is used, such as prohibiting certain renovations or limiting the number of occupants.

- Inability to sell or bequeath property: Once a portion or all of the property is sold through home reversion, the homeowner loses the ability to sell the property or pass it on to heirs.

Reduced Inheritance for Heirs

Another disadvantage of home reversion is that it can significantly reduce the inheritance that heirs receive. When a homeowner sells a portion or all of their property through home reversion, the value of the property is no longer part of their estate, which means there is less to pass on to heirs.

- Reduced estate value: Selling a portion or all of the property through home reversion reduces the overall value of the homeowner's estate, leaving less for heirs to inherit.

- Inability to pass on property: Once a portion or all of the property is sold, the homeowner loses the ability to pass it on to heirs as part of their inheritance.

- Potential for disputes among heirs: Home reversion can lead to disputes among heirs if they disagree with the decision to sell the property or feel they are not receiving their fair share of the inheritance.

Potential for Financial Loss

Home reversion can also result in a financial loss for homeowners if the value of the property decreases or if the homeowner lives longer than expected. If the property value decreases, the homeowner may receive less money than they anticipated. Additionally, if the homeowner lives longer than expected, they may end up receiving less money overall than if they had sold the property outright.

- Decreased property value: If the value of the property decreases after the home reversion transaction, the homeowner may receive less money than they anticipated.

- Longevity risk: If the homeowner lives longer than expected, they may end up receiving less money overall than if they had sold the property outright.

- Inflation risk: The lump sum or regular payments received from home reversion may lose value over time due to inflation, reducing the overall financial benefit to the homeowner.

What is a home reversion?

A home reversion is a type of equity release scheme that allows homeowners to access the value of their property without having to move out or sell it on the open market. This is achieved by selling a portion, or all, of their home to a home reversion provider in exchange for a tax-free lump sum or regular payments. The homeowner retains the right to live in the property for the rest of their life or until they move into long-term care.

How Home Reversion Works

Home reversion involves selling a percentage of your property to a provider in return for a lump sum or regular income. The amount you receive will be less than the market value of the share you sell, as the provider will offer a discounted price based on your age and life expectancy. You can continue living in your home rent-free until you pass away or move into long-term care, at which point the property is sold, and the provider receives their share of the proceeds.

- The homeowner decides to sell a portion or all of their property to a home reversion provider.

- The provider offers a lump sum or regular payments based on a discounted value of the share being sold.

- The homeowner retains the right to live in the property for the rest of their life or until they move into long-term care.

Advantages of Home Reversion

There are several benefits to choosing a home reversion plan, such as:

- Tax-free cash: The money received from a home reversion plan is tax-free, providing a financial boost to homeowners.

- No monthly repayments: Unlike traditional mortgages, home reversion does not require any monthly repayments, allowing homeowners to maintain their lifestyle.

- Guaranteed right to stay: Homeowners can continue living in their property for the rest of their life without the risk of eviction.

Disadvantages of Home Reversion

However, there are also some drawbacks to consider before entering into a home reversion plan:

- Reduced inheritance: As you are selling a portion of your property, the inheritance you leave behind will be reduced proportionately.

- Loss of property value: The amount received for the share of your property will be less than its market value, which can feel like a loss for some homeowners.

- Difficulty reversing the plan: If you change your mind, it can be difficult and costly to reverse a home reversion plan.

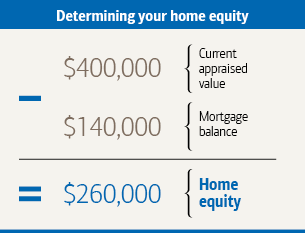

How to calculate equity release?

Equity release is a way for homeowners to access the value tied up in their property without having to sell it. It's a financial arrangement that allows individuals aged 55 and over to release tax-free cash from their homes. The amount that can be released depends on various factors, such as the value of the property, the age of the youngest homeowner, and the type of equity release plan chosen.

Equity Release Calculation Methods

There are two main types of equity release plans: lifetime mortgages and home reversion plans. The calculation of how much equity can be released varies between these two methods.

- Lifetime Mortgages: This is the most common type of equity release. The amount you can borrow depends on your age and the value of your property. Typically, the older you are, the more you can borrow. The interest on the loan is usually added to the amount borrowed, which means the debt can grow over time.

- Home Reversion Plans: With this plan, you sell a portion or all of your home to a home reversion provider in exchange for a lump sum or regular payments. You can continue living in the property rent-free until you die or move into long-term care. The amount you can release is based on the value of your property and your age, with older individuals typically receiving more.

- Equity Release Calculators: Many equity release providers offer online calculators that can give you an estimate of how much you could release from your property. These calculators take into account the value of your property, your age, and the type of equity release plan you're interested in.

Factors Affecting Equity Release

Understanding the factors that affect equity release can help you make an informed decision.

- Age: The age of the youngest homeowner is a significant factor in determining how much equity can be released. Generally, the older you are, the more you can release.

- Property Value: The value of your property also plays a crucial role. A higher property value usually means you can release more equity.

- Type of Plan: Lifetime mortgages and home reversion plans offer different amounts based on their terms and conditions. It's essential to understand which plan suits your needs best.

Considerations Before Releasing Equity

While equity release can be a useful way to access funds, there are important considerations to keep in mind.

- Impact on Inheritance: Equity release will reduce the value of your estate and the amount you can leave as inheritance.

- Interest Rates: For lifetime mortgages, the interest can significantly increase the amount you owe over time, especially if the interest is compounded.

- Early Repayment Charges: Some equity release plans may charge a fee if you decide to repay the loan early. It's important to understand these potential costs.

FAQ

What is a Home Reversion Calculator?

A Home Reversion Calculator is an online tool that helps you understand how much money you could potentially release from your property through a home reversion plan. This type of equity release allows homeowners to sell a portion or all of their property to a reversion company in exchange for a lump sum or regular payments, while still maintaining the right to live in the property rent-free for the rest of their lives.

How does a Home Reversion Calculator work?

A Home Reversion Calculator works by taking into account several factors about your property and personal circumstances. The calculator will typically ask for the value of your home, your age, and the percentage of your property you wish to sell. Based on these details, it calculates an estimate of the amount you could receive. However, it's essential to remember that the actual amount can vary depending on the specific terms of the home reversion plan and the provider you choose.

Why should I use a Home Reversion Calculator?

Using a Home Reversion Calculator is beneficial if you're considering a home reversion plan but are unsure about how much money you could release from your property. It provides a quick and easy way to get an estimate without having to commit to anything. It also allows you to compare different scenarios, such as selling different percentages of your property, to see how it affects the potential lump sum.

Is the estimate from a Home Reversion Calculator accurate?

While a Home Reversion Calculator can give you a rough estimate of the amount you could receive from a home reversion plan, it's not a guarantee. Many factors can influence the actual amount, including the specific terms of the plan, the provider's offer, and the current state of the property market. Therefore, it's crucial to speak with a financial advisor before making a decision. They can provide more detailed advice tailored to your personal circumstances and help you understand all the implications of a home reversion plan.

Deja una respuesta

Related article