Reverse Mortgage Alabama: Complete Guide and Calculator for Reverse Mortgages in Alabama

Reverse mortgage is becoming an increasingly popular option for homeowners in Alabama who are looking to supplement their retirement income. This financial tool allows seniors to convert a portion of their home equity into cash, without having to sell their property or take on additional monthly payments. If you're considering a reverse mortgage in Alabama, it's essential to understand how it works and what factors you need to consider before making a decision. This comprehensive guide will walk you through the process, explain the benefits and drawbacks, and provide you with a handy calculator to estimate your potential proceeds from a reverse mortgage in Alabama.

Understanding Reverse Mortgages in Alabama: A Comprehensive Guide and Calculator

Reverse mortgages are a unique financial tool that allows homeowners aged 62 and older to convert a portion of their home equity into cash. In Alabama, as in many other states, reverse mortgages can be a viable option for seniors looking to supplement their retirement income. This guide will provide a detailed overview of reverse mortgages in Alabama, including how they work, eligibility requirements, and the benefits and risks associated with them.

How Reverse Mortgages Work in Alabama

A reverse mortgage is a loan that allows homeowners to borrow against the equity in their home. Unlike a traditional mortgage, where the borrower makes monthly payments to the lender, a reverse mortgage does not require any payments until the borrower no longer lives in the home. The loan is repaid when the borrower sells the home, moves out, or passes away. In Alabama, reverse mortgages are available through the Federal Housing Administration's (FHA) Home Equity Conversion Mortgage (HECM) program. The HECM program is the most popular type of reverse mortgage and is insured by the federal government.

Eligibility Requirements for Reverse Mortgages in Alabama

To qualify for a reverse mortgage in Alabama, borrowers must meet the following requirements:

- Be at least 62 years old

- Own their home outright or have a low mortgage balance

- Live in the home as their primary residence

- Not be delinquent on any federal debt

- Have the financial resources to pay property taxes, insurance, and maintenance costs

Benefits of Reverse Mortgages in Alabama

Reverse mortgages offer several benefits for seniors in Alabama, including:

- Tax-free income: The funds received from a reverse mortgage are not considered taxable income.

- No monthly payments: Borrowers do not have to make monthly payments on the loan.

- Flexibility: The funds can be used for any purpose, such as paying for healthcare costs, home repairs, or daily living expenses.

- No risk of losing the home: As long as the borrower continues to live in the home and meet the loan requirements, they cannot be forced to sell the home to repay the loan.

Risks of Reverse Mortgages in Alabama

While reverse mortgages can be beneficial, there are also risks to consider:

- High fees: Reverse mortgages can come with high upfront costs, including origination fees, closing costs, and mortgage insurance premiums.

- Reduced equity: As the borrower receives payments, the equity in their home decreases, which can impact the inheritance left to heirs.

- Potential foreclosure: If the borrower fails to meet the loan requirements, such as paying property taxes and insurance, the lender can foreclose on the home.

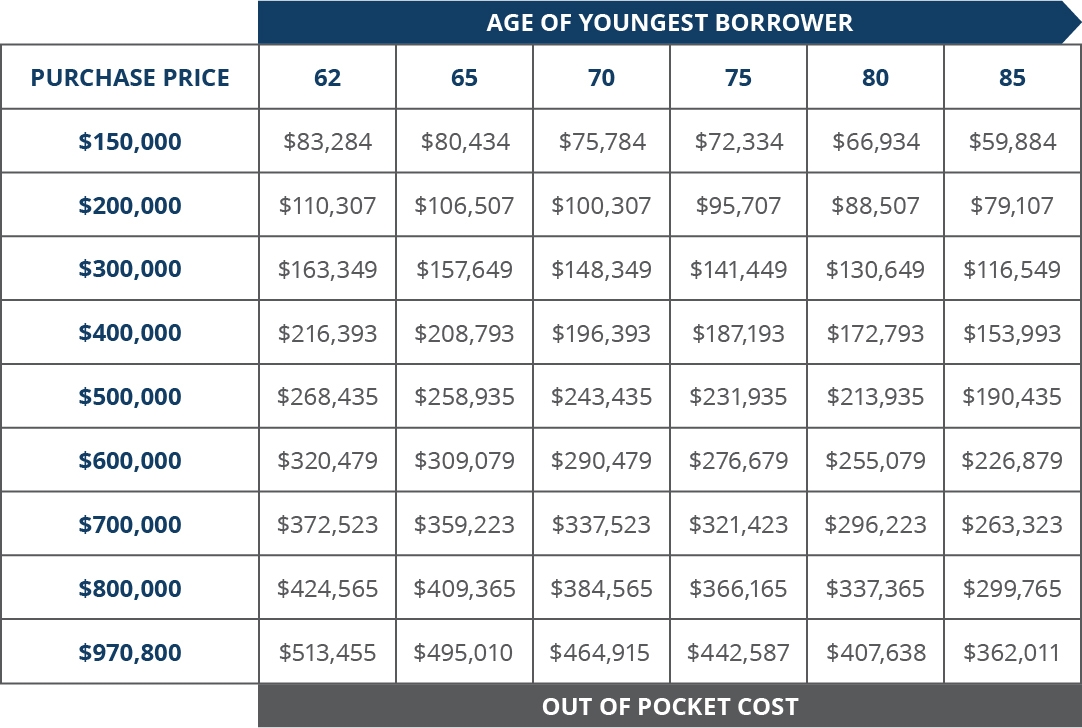

Reverse Mortgage Calculator for Alabama Homeowners

To determine how much you may be eligible to receive from a reverse mortgage, you can use a reverse mortgage calculator. The calculator will take into account factors such as your age, the value of your home, and current interest rates to provide an estimate of the funds you may receive.

| Factor | Description |

|---|---|

| Age | The older you are, the more funds you may be eligible to receive. |

| Home Value | The higher the value of your home, the more funds you may be eligible to receive. |

| Interest Rates | Lower interest rates can result in more funds being available to you. |

It's important to note that while a reverse mortgage calculator can provide an estimate, the actual amount you receive may differ based on your specific circumstances. It's always a good idea to consult with a financial advisor or reverse mortgage counselor before making a decision.

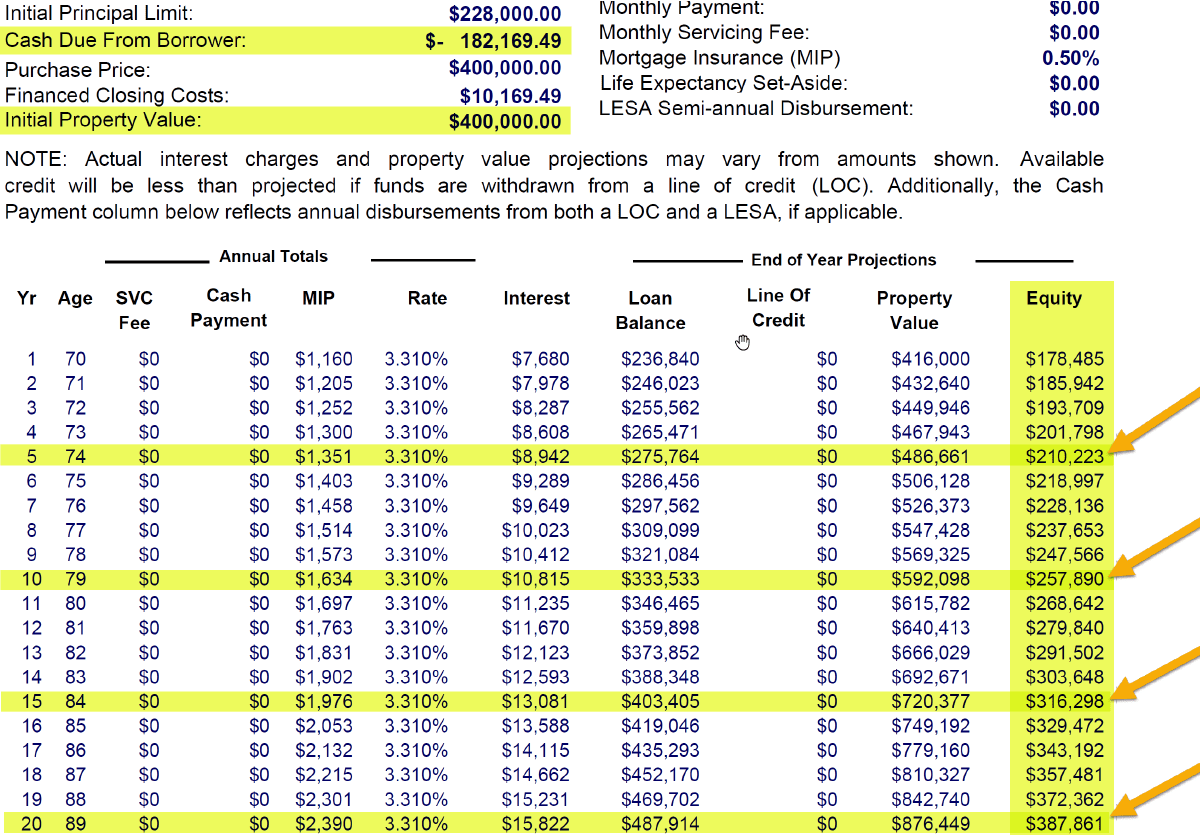

How is a reverse mortgage calculated?

A reverse mortgage is a type of loan that allows homeowners to convert a portion of their home equity into cash. The amount of money a borrower can receive depends on several factors, including the age of the youngest borrower, the current interest rate, and the appraised value of the home.

Factors Influencing Reverse Mortgage Calculation

The calculation of a strong{reverse mortgage} involves several key factors. These include:

- strong{Age of the Youngest Borrower:} The age of the youngest borrower on the loan is a significant factor. The older the borrower, the higher the loan amount they can receive.

- strong{Current Interest Rate:} The current interest rate influences the loan amount. Lower interest rates typically result in higher loan amounts.

- strong{Appraised Value of the Home:} The appraised value of the home is also a determining factor. The higher the value of the home, the higher the potential loan amount.

Process of Reverse Mortgage Calculation

The process of calculating a reverse mortgage involves a specific sequence of steps:

- strong{Appraisal:} The lender will appraise the home to determine its current market value.

- strong{Determine Interest Rate:} The lender will determine the current interest rate for the loan.

- strong{Calculate Loan Amount:} Based on the age of the youngest borrower, the current interest rate, and the appraised value of the home, the lender will calculate the maximum loan amount.

Types of Reverse Mortgage Payments

Borrowers can receive payments from a reverse mortgage in several ways:

- strong{Lump Sum:} A lump-sum payment is a one-time payment made at the closing of the loan.

- strong{Monthly Payments:} Borrowers can choose to receive fixed monthly payments for a set term or for as long as they live in the home.

- strong{Line of Credit:} A line of credit allows borrowers to withdraw funds as needed, up to a maximum amount.

How much can a 70 year old borrow on a reverse mortgage?

The amount a 70 year old can borrow on a reverse mortgage depends on several factors, including the value of the home, current interest rates, and the borrower's age. Generally, the older the borrower, the more they can borrow. As of 2021, the maximum lending limit for a Home Equity Conversion Mortgage (HECM), the most common type of reverse mortgage, is $822,375. However, the actual amount a 70 year old can borrow will likely be less than this limit.

Factors Affecting Reverse Mortgage Borrowing Limits

Several factors influence how much a 70 year old can borrow on a reverse mortgage:

- Home Value: The higher the appraised value of the home, the more the borrower can potentially access.

- Interest Rates: Lower interest rates generally allow for higher borrowing amounts.

- Borrower's Age: Older borrowers can typically borrow more than younger borrowers.

Calculating Reverse Mortgage Proceeds

To estimate how much a 70 year old can borrow, lenders use a formula that considers:

- Principal Limit Factor (PLF): Based on the borrower's age and current interest rates.

- Maximum Claim Amount (MCA): The lesser of the home's appraised value or the HECM lending limit.

- Mandatory Obligations: Any existing mortgage balance, closing costs, and other fees that must be paid off with the loan proceeds.

Example Scenario

Consider a 70 year old homeowner with a home valued at $500,000 and no existing mortgage:

- PLF: Based on age 70 and a 3% interest rate, the PLF might be around 0.50.

- MCA: The lesser of $500,000 or $822,375 is $500,000.

- Proceeds: $500,000 x 0.50 = $250,000, minus any closing costs and fees.

How much do you need for a down payment on a reverse mortgage?

To answer the question, , it's crucial to understand that a reverse mortgage fundamentally differs from a traditional mortgage, primarily because it doesn't require the homeowner to make monthly mortgage payments. Instead, it allows homeowners aged 62 and older to convert part of their home equity into cash. Therefore, the concept of a down payment in the context of reverse mortgages is somewhat misleading. Reverse mortgages are designed to provide money to the homeowner, not require an initial payment from them. However, there are costs associated with initiating a reverse mortgage, such as origination fees, closing costs, and mortgage insurance premiums, which can sometimes be paid upfront or rolled into the loan.

Understanding Reverse Mortgage Costs

While there's no down payment required in the traditional sense for a reverse mortgage, it's essential to consider the following costs which can be significant:

- Origination Fee: This fee compensates the lender for processing the reverse mortgage. It can vary but is capped by the federal government.

- Mortgage Insurance Premium (MIP): This is a fee paid to the Federal Housing Administration (FHA) to insure the loan. It's a significant cost that protects both the borrower and the lender if the loan balance grows to exceed the home's value.

- Closing Costs: Similar to traditional mortgages, these include various fees related to closing the loan, such as appraisal fees, title search, and insurance, surveys, inspections, and credit checks.

Eligibility Requirements for a Reverse Mortgage

Before considering the associated costs, it's vital to ensure you meet the eligibility criteria for a reverse mortgage:

- Age Requirement: The borrower must be at least 62 years old. If the homeowners are married, both must be at least 62 to be on the loan.

- Homeownership: The borrower must own the home outright or have a significant amount of equity in it.

- Primary Residence: The home must be the borrower's primary residence, meaning they live there for the majority of the year.

Types of Reverse Mortgages

Understanding the different types of reverse mortgages can help you comprehend the financial implications better:

- Home Equity Conversion Mortgages (HECMs): These are federally insured reverse mortgages backed by the U.S. Department of Housing and Urban Development (HUD). They are the most common type and have no income or medical requirements.

- Proprietary Reverse Mortgages: These are private loans backed by the companies that develop them. They might offer more substantial loan amounts for higher-valued homes.

- Single-Purpose Reverse Mortgages: Offered by some state and local government agencies and nonprofits, these are the least expensive option but can be used for only one purpose, specified by the lender.

How does a reverse mortgage work in Alabama?

A reverse mortgage in Alabama is a type of loan that allows homeowners who are 62 years of age or older to convert part of their home equity into cash. Unlike a traditional mortgage where the homeowner makes payments to the lender, in a reverse mortgage, the lender makes payments to the homeowner. The loan is repaid when the homeowner sells the home, moves out, or passes away.

Eligibility Requirements

To qualify for a reverse mortgage in Alabama, you must meet the following criteria:

- You must be at least 62 years old.

- You must own your home outright or have a low mortgage balance that can be paid off with the proceeds from the reverse mortgage.

- You must live in the home as your primary residence.

- You must not be delinquent on any federal debt.

- You must have the financial resources to pay ongoing property taxes, insurance, and home maintenance costs.

Types of Reverse Mortgages

There are three main types of reverse mortgages available in Alabama:

- Home Equity Conversion Mortgages (HECMs): These are federally-insured reverse mortgages backed by the U.S. Department of Housing and Urban Development (HUD).

- Proprietary Reverse Mortgages: These are private loans offered by banks and mortgage companies. They are not federally insured and may have higher fees and interest rates than HECMs.

- Single-Purpose Reverse Mortgages: These loans are offered by state and local government agencies and nonprofit organizations. They are typically used for a specific purpose, such as home repairs or property taxes.

Repayment and Risks

A reverse mortgage must be repaid when the homeowner sells the home, moves out, or passes away. The loan balance includes the amount borrowed, plus interest and fees. If the home is sold, the proceeds from the sale are used to pay off the loan. If the loan balance exceeds the home's value, the lender may seek repayment from the homeowner's other assets.

- The loan balance grows over time as interest and fees accumulate.

- The homeowner is responsible for paying property taxes, insurance, and maintenance costs.

- Reverse mortgages can affect the homeowner's eligibility for Medicaid and other need-based government programs.

FAQ

What is a Reverse Mortgage and how does it work in Alabama?

A Reverse Mortgage is a type of loan that allows homeowners, aged 62 or older, to convert part of their home equity into cash. Unlike a traditional mortgage where the homeowner makes payments to the lender, in a reverse mortgage, the lender makes payments to the homeowner. The loan is repaid when the homeowner sells the home, moves out, or passes away. In Alabama, the most common type of reverse mortgage is the Home Equity Conversion Mortgage (HECM), which is insured by the Federal Housing Administration (FHA). The amount you can borrow depends on your age, the current interest rate, and the appraised value of your home.

Who is eligible for a Reverse Mortgage in Alabama?

To be eligible for a Reverse Mortgage in Alabama, the homeowner must be at least 62 years old and own their home outright or have a low mortgage balance that can be paid off at closing with proceeds from the reverse loan. The home must be the applicant's primary residence and must meet all FHA property standards and flood requirements. Additionally, the homeowner must have the financial resources to pay ongoing property taxes, insurance, and home maintenance costs, and they must participate in a consumer information session given by a HUD-approved HECM counselor.

How can a Reverse Mortgage Calculator help me?

A Reverse Mortgage Calculator can help you estimate the total amount of proceeds you may receive from a reverse mortgage. The calculator takes into account your age, your spouse's age (if applicable), the value of your home, the current interest rate, and your zip code. By inputting this information, the calculator can give you an estimate of the total amount of money you could receive, both initially and over time if you choose to receive monthly disbursements. This tool is useful for planning purposes, but remember that the actual amount you receive may differ.

What are the pros and cons of getting a Reverse Mortgage in Alabama?

The pros of getting a Reverse Mortgage in Alabama include the ability to supplement your retirement income, pay off your existing mortgage, or cover other expenses. The funds can be received as a lump sum, line of credit, or monthly payments, and the loan does not need to be repaid until you sell your home or pass away. However, there are also cons to consider. These include the high upfront costs, the fact that the loan balance increases over time and can deplete your home equity, and the possibility that you could lose your home if you do not meet the loan requirements like paying property taxes and homeowner’s insurance. It's crucial to consider both the advantages and disadvantages and consult with a financial advisor before making a decision.

Deja una respuesta

Related article