Reverse Mortgage Arkansas: Reverse Mortgage Guide for Arkansas Homeowners

Arkansas homeowners seeking financial flexibility in their golden years may find a reverse mortgage to be an attractive option. A reverse mortgage allows homeowners aged 62 and older to convert a portion of their home equity into cash, providing a valuable source of income while still maintaining ownership of their property. This comprehensive guide will explore the ins and outs of reverse mortgages in Arkansas, including eligibility requirements, benefits, potential drawbacks, and the application process. By understanding how reverse mortgages work and what to consider, Arkansas homeowners can make informed decisions about whether this financial tool aligns with their retirement goals.

Understanding Reverse Mortgages in Arkansas: A Comprehensive Guide for Homeowners

Reverse mortgages are a unique financial product that allows homeowners aged 62 and older to convert a portion of their home equity into cash. Arkansas residents who are considering a reverse mortgage should understand the details of these loans, their benefits, and the potential risks involved. In this guide, we'll cover the essentials of reverse mortgages in Arkansas.

Eligibility Requirements for Reverse Mortgages in Arkansas

To qualify for a reverse mortgage in Arkansas, you must meet certain criteria:

- You must be at least 62 years old.

- You must own your home outright or have a low mortgage balance that can be paid off with the proceeds from the reverse mortgage.

- You must live in the home as your primary residence.

- Your home must meet all FHA property standards and flood requirements.

- You must have the financial resources to continue making timely payment of property taxes, homeowners insurance, HOA fees, etc.

Types of Reverse Mortgages Available in Arkansas

There are three main types of reverse mortgages available to Arkansas homeowners:

- Home Equity Conversion Mortgage (HECM): This is the most common type of reverse mortgage and is insured by the Federal Housing Administration (FHA). It can be used for any purpose and offers various disbursement options.

- Proprietary Reverse Mortgages: These are private loans not backed by the government. They may offer higher loan amounts for homeowners with high-value homes.

- Single-Purpose Reverse Mortgages: These loans are typically offered by state and local government agencies or nonprofit organizations. They are used for specific purposes, such as home repairs or property taxes.

Benefits of Reverse Mortgages for Arkansas Homeowners

Reverse mortgages offer several potential benefits, including:

- Supplemental Income: You can receive loan proceeds as a lump sum, monthly payments, or a line of credit, providing additional income during retirement.

- No Monthly Mortgage Payments: With a reverse mortgage, you are not required to make monthly mortgage payments. The loan is repaid when you sell the home, move out permanently, or pass away.

- Flexibility: You can use the funds from a reverse mortgage for any purpose, such as home improvements, medical expenses, or daily living costs.

- Non-Recourse Loan: A reverse mortgage is a non-recourse loan, meaning you or your heirs will never owe more than the value of your home when the loan becomes due.

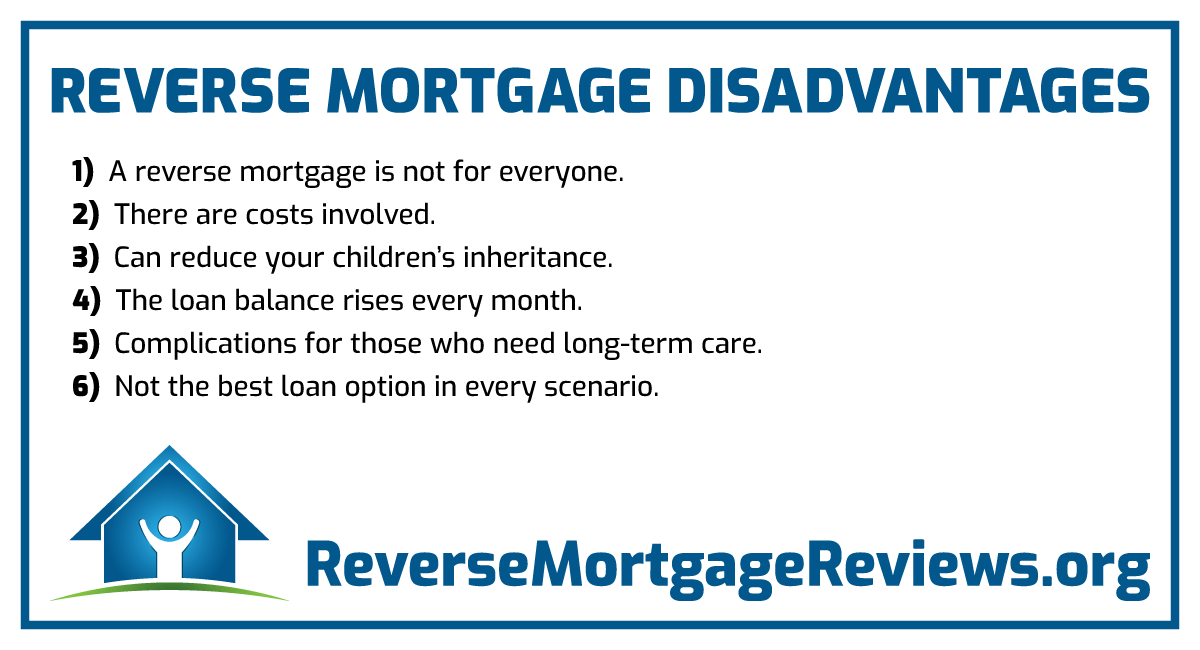

Potential Risks of Reverse Mortgages in Arkansas

While reverse mortgages can be beneficial, there are also potential risks to consider:

- Costs and Fees: Reverse mortgages can have high upfront costs and ongoing fees, such as origination fees, mortgage insurance premiums, and servicing fees.

- Impact on Inheritance: When the loan becomes due, your heirs may need to sell the home to repay the loan, reducing the inheritance they receive.

- Responsibility for Property Charges: You are still responsible for paying property taxes, homeowners insurance, and maintenance costs. Failure to do so could result in foreclosure.

Frequently Asked Questions about Reverse Mortgages in Arkansas

| Question | Answer |

|---|---|

| How much can I borrow with a reverse mortgage in Arkansas? | The amount you can borrow depends on factors such as your age, the appraised value of your home, current interest rates, and the type of reverse mortgage you choose. |

| Is there a minimum credit score required for a reverse mortgage in Arkansas? | No, there is no minimum credit score requirement for a reverse mortgage. However, lenders will conduct a financial assessment to ensure you can meet your ongoing obligations. |

| Can I lose my home with a reverse mortgage? | You will not lose your home as long as you continue to meet the loan requirements, such as living in the home as your primary residence and paying property taxes and insurance. |

What is the 60% rule for reverse mortgage?

The 60% rule for reverse mortgage is a guideline established by the Federal Housing Administration (FHA) to ensure that borrowers do not overextend themselves financially. This rule states that in the first year of the loan, borrowers can only access up to 60% of the total loan amount. This is done to protect the borrower from using up all their equity too quickly and to ensure that they have sufficient funds for living expenses, taxes, and insurance.

Reasons for the 60% Rule

The 60% rule exists for several reasons:

- Financial Protection: It helps to prevent borrowers from spending all their equity at once, which could leave them without sufficient funds for their living expenses.

- Tax and Insurance: The rule ensures that the borrower has enough money to pay for property taxes and homeowners insurance.

- Loan Sustainability: It helps to ensure that the loan will last for the duration of the borrower's life or until they move out of the home.

Exceptions to the 60% Rule

There are some exceptions to the 60% rule:

- Mandatory Obligations: If the borrower has mandatory obligations such as mortgage payments or other liens, these must be paid off with the loan proceeds, even if this exceeds the 60% limit.

- Non-Borrowing Spouse: If there is a non-borrowing spouse, the 60% rule may be adjusted to ensure that the spouse has sufficient funds to live on after the borrower's death.

Accessing More Than 60%

After the first year, borrowers may be able to access more than 60% of the loan amount:

- Additional Funds: If the borrower needs more than 60% of the loan amount after the first year, they can request additional funds. However, they must demonstrate that they can afford to pay the additional costs associated with the loan.

- Loan Terms: The borrower must also meet all the terms of the loan, including maintaining the home as their primary residence and keeping up with taxes and insurance.

How much do you need for a down payment on a reverse mortgage?

When it comes to reverse mortgages, the concept of a down payment doesn't apply in the traditional sense. Unlike a regular mortgage where you make monthly payments to a lender, a reverse mortgage pays you. The amount you can borrow depends on several factors including your age, the appraised value of your home, and current interest rates.

Eligibility Requirements for a Reverse Mortgage

To qualify for a reverse mortgage, you must meet certain criteria. You must be 62 years or older, own your home outright or have a low mortgage balance that can be paid off with the proceeds from the reverse mortgage. Additionally, you must live in the home as your primary residence and not be delinquent on any federal debt.

- Age Requirement: You must be at least 62 years old.

- Home Ownership: You must own your home outright or have a low mortgage balance.

- Primary Residence: You must live in the home as your primary residence.

Costs Associated with a Reverse Mortgage

While there's no down payment required for a reverse mortgage, there are costs involved. These include origination fees, closing costs, and mortgage insurance premiums. These costs can be paid upfront or rolled into the loan balance.

- Origination Fees: These are fees charged by the lender to cover the cost of processing the loan.

- Closing Costs: These include appraisal fees, title search, and insurance, among others.

- Mortgage Insurance Premiums: These are paid to the Federal Housing Administration to insure the loan.

How Much Can You Borrow?

The amount you can borrow with a reverse mortgage depends on several factors including your age, the value of your home, and current interest rates. Generally, the older you are and the more valuable your home is, the more you can borrow. However, there are limits set by the Federal Housing Administration.

- Age: The older you are, the more you can potentially borrow.

- Home Value: The more your home is worth, the more you can potentially borrow.

- Interest Rates: Lower interest rates can increase the amount you can borrow.

What is the negative side of a reverse mortgage?

The negative side of a reverse mortgage primarily revolves around the costs and potential risks associated with this type of loan.

High Costs and Fees

One of the significant downsides of reverse mortgages is the high costs and fees involved. These can include origination fees, mortgage insurance premiums, and closing costs.

- Origination Fees: Lenders charge these fees for processing the loan. They can be high, often a percentage of the home's value.

- Mortgage Insurance Premiums: Borrowers are required to pay these premiums, which protect the lender if the borrower fails to meet the loan terms.

- Closing Costs: These include various fees similar to those in a traditional mortgage, such as appraisal, title insurance, and inspection fees.

Potential Impact on Estate and Inheritance

A reverse mortgage can significantly impact the homeowner's estate and inheritance. The loan balance increases over time as interest and fees accumulate, which can reduce the equity in the home.

- Reduced Inheritance: As the loan balance grows, it may consume most or all of the home's equity, leaving less value for heirs.

- Repayment Responsibility: When the homeowner passes away or moves out, the loan becomes due. Heirs may need to sell the home to repay the loan, which can be a burden.

- Potential Foreclosure: If the loan terms are not met (e.g., maintaining the home, paying property taxes and insurance), the lender can foreclose on the home.

Potential for Scams and Misunderstandings

Reverse mortgages can be complex, leading to potential scams or misunderstandings. Some lenders or advisors may not fully explain the risks or may even engage in fraudulent practices.

- Misleading Advertising: Some advertisements may make reverse mortgages sound more appealing than they are, without adequately explaining the risks.

- High-Pressure Sales Tactics: Some lenders may use high-pressure tactics to encourage borrowers to take out a reverse mortgage, even if it's not in their best interest.

- Potential Fraud: Scammers may target seniors with schemes related to reverse mortgages, such as fraudulent home repairs or investment opportunities.

FAQ

What is a reverse mortgage and how does it work in Arkansas?

A reverse mortgage is a type of loan that allows homeowners aged 62 or older to convert part of their home equity into cash without having to sell their home or pay additional monthly bills. In Arkansas, like in the rest of the United States, the most common type of reverse mortgage is the Home Equity Conversion Mortgage (HECM), which is insured by the Federal Housing Administration (FHA). The loan amount is based on the age of the youngest borrower, the current interest rate, and the appraised value of the home. The loan does not have to be repaid until the last surviving homeowner permanently moves out of the property or passes away, at which point the estate has approximately 6 months to repay the balance of the reverse mortgage or sell the home to pay off the balance.

What are the requirements to qualify for a reverse mortgage in Arkansas?

To qualify for a reverse mortgage in Arkansas, the homeowners must be at least 62 years old, own their home outright or have a low mortgage balance that can be paid off at closing with proceeds from the reverse mortgage, and live in the home as their primary residence. Additionally, the homeowners must not be delinquent on any federal debt, and they must have the financial resources to continue to pay property taxes, insurance, and maintain the home. The property must also meet FHA minimum property standards and flood requirements. It's also mandatory for homeowners to receive counseling from a HUD-approved counseling agency.

How can the funds from a reverse mortgage be used?

The funds from a reverse mortgage can be used for any purpose. Many homeowners use the funds to supplement retirement income, pay for health care expenses, make home improvements, or pay off existing debts. The funds can be received in a lump sum, monthly payments, a line of credit, or a combination of these. The initial mortgage insurance premium is based on the amount of funds withdrawn during the initial year.

What happens if the loan amount exceeds the value of the home?

Reverse mortgages are non-recourse loans, which means that if the loan amount exceeds the value of the home when the loan becomes due, the homeowner or their heirs will never owe more than the loan balance or the value of the property, whichever is less. If the home is sold for less than the balance of the reverse mortgage, the insurer (typically the Federal Housing Administration) will cover the difference. This feature protects the homeowner and their estate from owing more than the home is worth.

Deja una respuesta

Related article